Survival of the Licensed

Inside the MiCA cull: how Europe went from 3,167 crypto firms to 244 in eighteen months.

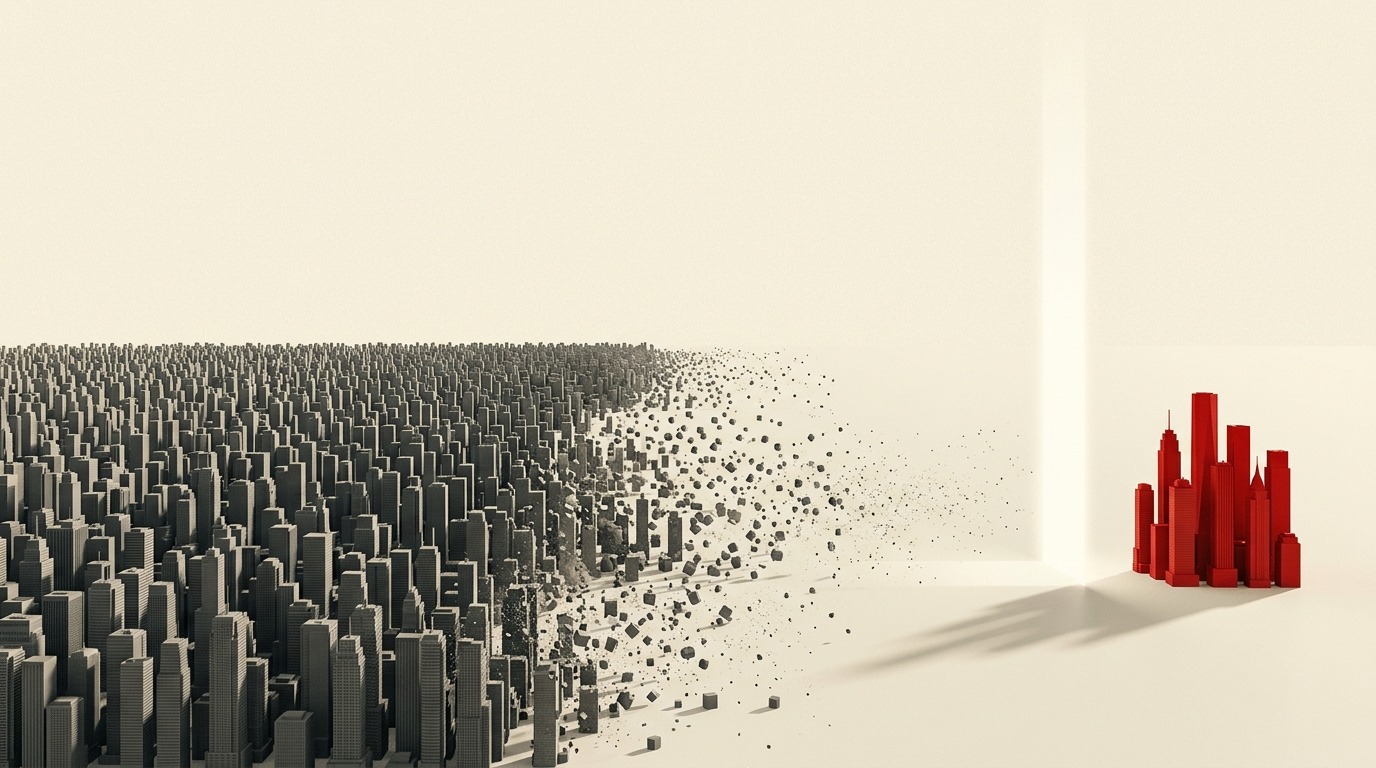

On July 1, 2026, the transitional window under the EU's Markets in Crypto-Assets Regulation closed with no extension. When it did, 244 firms held a full CASP licence. Before MiCA, more than three thousand entities operated across Europe under national registrations. The market did not collapse overnight, because most casualties were small and had been winding down for months. But the structure of European crypto changed permanently. It is now smaller, far more concentrated (nearly a quarter of all licences sit in Germany), and openly split between a licensed core and an offshore market that will keep serving EU users from a distance. The world's largest exchange and its largest stablecoin are both on the wrong side of the line.

This piece lays out the numbers, the geography, who survived and in what shape, what happens next to those who did not, and why the rulebook everyone just raced to meet is already being rewritten.

What actually happened on July 1

MiCA has been law since 2023, but it arrived in stages. The rules for stablecoin issuers took effect in mid-2024; the rules for crypto service providers (the exchanges, brokers, custodians and wallet apps) took effect at the end of 2024. To avoid shutting down a functioning market on day one, the regulation gave existing firms a grandfathering window. A company already licensed under a national regime could keep operating under those old rules until it received a MiCA licence, was refused one, or hit a hard cut-off. That cut-off was July 1, 2026.

The European Securities and Markets Authority removed any remaining ambiguity in an April statement: the transitional period ends July 1 across all 27 member states, with no mechanism to extend it. After that date the legal position is binary. A firm either holds a MiCA authorisation or it is providing crypto-asset services in breach of EU law. There is no "pending" status that lets a company keep trading while its paperwork is reviewed; an application on a regulator's desk confers no right to serve clients.

There is no intermediate status after July 1. A firm is either authorised under MiCA or it is in breach of EU law.

The deadline was never uniform, which is a detail most coverage misses. Member states could shorten the window, and several did. The Netherlands, Finland, Latvia, Hungary and Slovenia set six-month periods that closed back on June 30, 2025. Sweden ran nine months. Germany and Ireland used a twelve-month window that closed on December 31, 2025. France, Malta, Luxembourg and Estonia took the full eighteen months, which is what expired on July 1. So for a meaningful slice of the EU the cull happened months ago and went largely unremarked. July 1 was simply the last and largest domino.

The numbers behind the cull

The headline figure being repeated across the industry is that only about 17% of firms converted. It is directionally right but worth handling with care, because the denominator does most of the work.

The numerator is now firm. Public mirrors of ESMA's interim register, synced just after the deadline, put the total at 244 authorised CASPs across 25 home jurisdictions. Alongside them sit 20 authorised e-money-token (stablecoin) issuers and, strikingly, zero authorised asset-referenced-token issuers. Not a single multi-asset stablecoin cleared MiCA's reserve and governance bar.

The denominator is where sources diverge. Coincub counted roughly 3,167 national VASP registrations across Europe before MiCA. Measured against that base, 244 authorised firms is a 7.7% survival rate. Use a narrower base of around 1,200 formally registered VASPs and the rate rises to roughly 20%. Neither is wrong; they answer different questions. And a third cut complicates both: a cleaned April snapshot by Finray found that of 177 successful authorisations, only 47 were legacy VASPs that converted; the rest were banks, e-money institutions, investment firms using MiCA's simplified notification route, or crypto-native new entrants. In other words, the licensed market is not simply the old market with fewer names on it. It is a different population, tilted toward incumbents with existing regulatory infrastructure.

| Population measured | Authorised | Implied survival |

|---|---|---|

| Pre-MiCA national VASP registrations (~3,167) | 244 CASPs | ~7.7% |

| Formally registered VASPs (~1,200) | 244 CASPs | ~20% |

| E-money-token (stablecoin) issuers | 20 authorised | n/a |

| Asset-referenced-token issuers | 0 authorised | None cleared the bar |

Whatever base you choose, the direction is the same: the overwhelming majority of firms that once served European crypto users under national rules are not licensed to do so under MiCA. What that means in practice depends on which of three buckets a firm falls into: it cleared the bar, it is mid-process with no legal standing to keep trading, or it never intended to comply and will keep reaching EU users from outside the perimeter.

The geography of survival

Survival was not distributed evenly, and the concentration is the story. Germany alone accounts for 57 of the 244 licences, about 23% of the bloc, more than double second-placed France and the Netherlands, which sit level at 26 each. The reason is structural. A MiCA licence issued in one member state can be "passported" into all 27, but the country a firm licenses in becomes its home supervisor for the life of the licence, setting its capital expectations and its speed to market. Firms voted overwhelmingly for BaFin's predictability and the depth of the German market; Germany is also the top passporting hub by a wide margin.

At the other end of the map, five EU member states issued no CASP authorisations at all: Greece, Hungary, Poland, Portugal and Romania. Poland is the most telling case. Historically a popular hub under the old VASP regime, it simply could not license anyone, because the domestic law needed to implement MiCA was repeatedly vetoed by the Polish president and a parliamentary override narrowly failed. Firms domiciled there were forced to scramble and redomicile elsewhere in the EU. It is a sharp illustration of a structural weakness: a single market policed by 27 regulators of very different capacity and appetite is only as uniform as its slowest member, and some observers already argue the passport is fragmenting as firms shop for the fastest, cheapest home supervisor.

The scramble to the deadline

The licensed cohort is not only concentrated by geography; it is concentrated in time. Authorisations trickled through 2025 and then surged as the cut-off approached. There were around 102 CASPs by the end of December 2025, 177 by late April 2026, 206 by the start of June, 243 by June 27, and 244 by July 2. Put differently, more than a third of the entire licensed market was authorised in the final ten weeks, and the register was still moving in the last days before the window shut.

A last-minute bulge like this has consequences. Regulators processed a large share of approvals under deadline pressure, and firms that filed late but complete applications were left in limbo, legally unable to trade past July 1 even if their paperwork was sound, because pending status confers no rights. Some of the attrition, in other words, is not a judgement that a firm was unfit; it is a function of queue position. That distinction matters for how the next year plays out, because a firm refused on the merits is gone, while a firm caught in the queue is a live candidate to be licensed, acquired, or absorbed later.

What kind of firm survived

The service-level breakdown reveals what MiCA actually rewarded. Custody and administration is the most widely held authorisation, carried by around 160 of the 244 firms, a direct reflection of MiCA's emphasis on asset segregation and safekeeping. Exchange services (crypto-to-fiat and crypto-to-crypto) and the two brokerage functions cluster in the 84–100 range. Advice is rarer. And the operation of a full order-book trading platform (the licence a matching-engine exchange needs) was granted to just 14 firms across the entire bloc.

That final number is the sharpest signal in the dataset. Running a trading venue carries the heaviest technical, surveillance and cybersecurity obligations under MiCA, and only fourteen operators were willing and able to meet them. The practical effect is that the most systemically important layer of European crypto, the venues where price is actually formed, now runs through a very small number of licensed hands. Concentration at the custody and trading-venue level is exactly what a regulator focused on consumer protection was aiming for, but it also means resilience now depends on a short list of firms.

Who cleared the bar

The survivors are, for the most part, the platforms EU users already recognise. Among the largest exchange brands, register-based trackers show Coinbase, Kraken, OKX, Bybit, Gate, KuCoin, Bitstamp, Bitvavo, Crypto.com, Bitpanda, eToro, Revolut and Robinhood all holding authorised EU entities. On the stablecoin side, Circle is the standout: it holds MiCA authorisation for both USDC and its euro-denominated EURC, and among the top ten stablecoins by value it is the only issuer that cleared the bar. Société Générale-Forge (EURCV), Banking Circle (EURI), Quantoz and Membrane Finance (EUROe) round out a small field of mostly bank- and EMI-issued euro tokens. A day before the deadline, BNY made USDC the first stablecoin on its digital-asset custody platform, a signal of where regulated institutional flow is heading.

For this licensed core, MiCA is a moat. They now operate across a 450-million-person single market under one rulebook, with a compliance cost smaller rivals cannot easily match and a licence that doubles as a trust signal to banks and institutional counterparties. That is precisely the outcome the regulation was designed to produce.

Who did not

The two most visible casualties are not obscure firms. They are Binance and Tether, the largest exchange and the largest stablecoin in the world, and they represent two different kinds of loss.

Binance wanted in and could not close it. It pursued a licence through Greece's Hellenic Capital Market Commission and withdrew the application on June 24, days before the deadline; founder Changpeng Zhao's account is that two member states competed to host the bid before political opposition triggered the withdrawal. The outcome is concrete: Binance halted new EU registrations and told users in France, Italy, Poland and Spain that services would be restricted. Register trackers also mark Upbit, MEXC and Bitget as unlicensed. Binance's exit reads as a licensing failure, tangled up in national politics, and one that could reverse if it secures approval later.

Tether made the opposite choice. It never applied for the e-money-token authorisation MiCA requires, arguing through CEO Paolo Ardoino that the rule to hold 60% of reserves in European bank deposits introduces risk rather than removing it, and it decided to prioritise markets outside the EU rather than restructure. Licensed European exchanges have therefore delisted USDT, cutting the EU's regulated venues off from roughly $185 billion of the world's most-traded stablecoin. Tether's exit is a deliberate strategic bet, not an accident of timing: a structural gap rather than a temporary one. USDT will not return to licensed EU venues unless Tether restructures or MiCA's rules soften, and, as the last section notes, the latter is now genuinely on the table.

What happens to the firms that missed

For the firms now outside the perimeter, MiCA is prescriptive about the exit. Unlicensed firms are not simply switched off; they may perform only the activities needed to wind down in an orderly way, and ESMA has been explicit that credible wind-down plans were meant to be in place by July 1. In practice that means four things.

- Stop onboarding. No new EU clients, no new positions, the first thing to go, and most affected firms did it weeks ahead.

- Offboard existing clients. Users must be notified and given a route out: transfer to an authorised CASP or withdraw to a self-hosted wallet.

- Transfer or return custody. Customer assets have to move somewhere legal, which is why analysts expect a rush toward licensed custody providers.

- Close out. Once clients are offboarded, the EU-facing entity ceases regulated activity or restructures around a licensed partner.

For users, the practical risk is not that funds are seized on July 1 but that access narrows abruptly. A wind-down done well is quiet; a wind-down done badly, a small firm that runs out of money before it finishes offboarding, is where customers get hurt, and it is the scenario regulators are watching most closely. There is also a leak the rules cannot fully close: when a platform tells users to move to a licensed CASP or a self-hosted wallet, a share of them will simply re-onboard at whichever offshore venue still accepts them. Regulators can compel the exit of the domestic entity; they cannot easily compel where a user's assets land next.

The consolidation wave

The most durable market effect is consolidation, running in two directions. The first is a custody-and-infrastructure land grab: smaller apps and brokers that cannot justify their own licence increasingly plug into a licensed firm's rails, holding customer assets through an authorised custodian and effectively renting compliance. That pushes value toward a small number of licensed infrastructure providers and makes regulated custody one of the more attractive businesses in European crypto.

The second is outright M&A. A licence is now a scarce, valuable asset, and the fastest way to acquire one is to buy a firm that already holds it, or to buy the client book of a firm that is winding down. Analysts expect deal activity to accelerate through the second half of 2026, concentrated among mid-sized firms that lack the capital to meet MiCA's standards alone. Some genuinely good companies, unable to get licensed in time, become acquisition targets rather than failures. The end state is a smaller, more concentrated market with higher barriers to entry, fewer independent players and, the intended trade-off, stronger consumer protections and clearer institutional on-ramps.

It is tempting to read the licensed cohort as pure winners, but the moat carries a cost. A MiCA licence brings ongoing obligations: minimum capital, governance and custody standards, complaints handling, market-abuse monitoring, continuous reporting. A large exchange absorbs those easily; a mid-sized firm that scraped over the line carries a permanent drag that a lightly regulated offshore rival does not. The licensed market is therefore not just smaller but structurally more expensive to operate in, which is why the count of independent CASPs is likely to keep falling through acquisition even now that the deadline has passed. Survival was the entry ticket, not the finish line.

The enforcement reality

A rule is only as real as its enforcement, and here the picture is firm on paper and uneven in practice. National regulators are the enforcers, and the tone-setters have signalled no leniency: Spain's CNMV explicitly ruled out exceptions or extensions, and ESMA has said supervisors are expected to act against firms that keep serving clients without authorisation. The complication is capacity. With five member states yet to issue a single licence (Poland unable to even process applications), the supervisory muscle behind MiCA varies enormously by country. Enforcement against a domestically incorporated unlicensed firm is straightforward; enforcement against an offshore platform still reachable through a website and an app is a different problem, and the one MiCA cannot fully solve. The likely equilibrium is a clean, well-policed licensed core beside a persistent offshore grey market EU users can still reach with a little friction. MiCA reshapes the compliant market; it does not abolish the non-compliant one.

The rulebook is already being rewritten

The final twist is that MiCA reached its hardest deadline in the same week the European Commission opened a formal review of the regulation itself. A public consultation on what the industry calls "MiCA 2.0" runs through August 31, 2026, and it targets exactly the areas the current text handles awkwardly: the stablecoin rules, including the ban on paying interest and the reserve requirements that kept Tether out; the treatment of DeFi, which sits largely outside MiCA today; and how to bring real-world-asset tokenisation and staking formally into scope.

The catch is timing. Industry estimates put actual legislative proposals no earlier than 2028. So firms have just absorbed the cost of complying with a rulebook regulators openly concede needs updating, and the parts most relevant to where the market is heading (stablecoins, tokenisation, DeFi) are the parts still unsettled. Whatever moat today's licensees just built, the ground under it will shift again before the decade is out.

What to watch

Five things will show, over the second half of 2026, whether the cull produced a healthier market or merely a smaller one. Whether wind-downs stay orderly or a few undercapitalised firms fail messily. How many winding-down firms and client books get absorbed, and at what valuations, now that a licence is the asset worth buying. How much EU volume quietly migrates to non-compliant venues: the clearest measure of whether MiCA changed behaviour or just addresses. Whether USDC and EURC consolidate the compliant liquidity USDT vacated, and whether any ART issuer ever clears the bar. And the early direction of the MiCA 2.0 consultation, especially on the stablecoin interest ban, which will decide whether Europe stays a hard market for issuers or reopens the door.

The headline, more than nine in ten firms gone against the widest base, is dramatic, but the more accurate reading is that Europe traded breadth for order. It now has a licensed, passportable, institution-ready core of 244 firms, and it paid for that with a long tail of small operators and with the absence of the world's largest exchange and largest stablecoin from its regulated venues. Whether that was a fair price is the debate the next eighteen months, and MiCA 2.0, will settle.

Sources

- ESMA: Markets in Crypto-Assets Regulation (MiCA) and the public statement on the end of the transitional period.

- Register mirrors: CASPTracker and the Helms Advisory CASP licence tracker (244 CASPs, 20 EMT issuers, 0 ART issuers, synced July 2, 2026).

- Coincub Europe Crypto Report 2026 (about 3,167 pre-MiCA registrations).

- Finray CASP licensing analysis (47 of 177 successful authorisations were converted VASPs).

- CoinDesk: Binance withdraws its Greek MiCA bid, Europe's unlicensed firms face wipeout, and Europe rewrites the rulebook as the deadline passes.

- The Block: who wins and loses under MiCA.

- BeInCrypto: Circle as the MiCA stablecoin winner.

Notes. The 244 total is a post-deadline register read and may differ slightly from the exact supervisory figure. "Survival rate" is not an official metric; both the roughly 7.7% (base 3,167) and roughly 20% (base about 1,200) framings are shown deliberately. Service-type counts are approximate, from late-June registry analyses.